|

Executive Summary

|

Technical ProcessInvestment discipline helps manage risks and maintain decision-making consistency, ensuring alignment with long-term goals and reducing emotional biases. Incorporating trend indicators and understanding price dispersion have been key in timing investments and identifying undervalued assets, aiding in portfolio diversification.

However, relying on historical data for these strategies doesn't always predict future market behavior, and the market's efficiency can limit their effectiveness. These strategies also add complexity and costs, with risks of overfitting to past data and challenges in market timing. We also noticed that extreme dispersion does not always result in price movement back to the mean because of persistent trends that may develop. Instead of positioning solely on oversold/overbought signals, our work shows that blending indicators such as momentum, trend, and dispersion can help optimize investment strategies. While there are merits to trend following over the long-term, brief periods of volatility can increase drawdown risks. Mean reversion strategies can take advantage of wide dispersion in asset returns as trends weaken, albeit short-term. This was evident in the recent rally in US small-cap stocks, price corrections in some industrial metals, and a rise in equity volatility. Therefore, we recognize the importance of adapting strategies to various market environments. Disclaimer: The Content is for informational purposes only and does not reflect holdings. Information or other material is not investment advice.

|

|

MACD/RSI Model

|

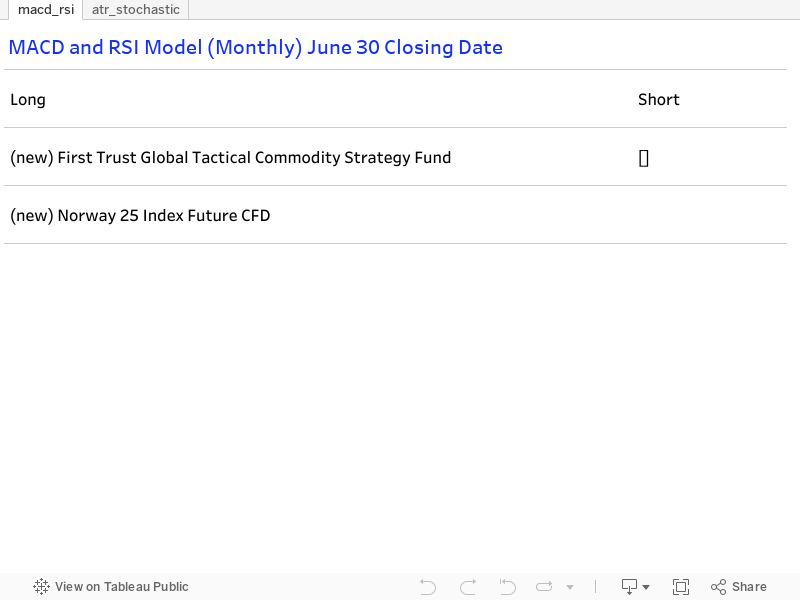

Trend & MomentumThe MACD/RSI model, developed by Kyaw Swar Ye Myint, is designed to provide a comprehensive assessment of market trends and momentum. Instead of relying solely on an overbought/oversold indicator, the model attempts to measure renewed price strength within an existing bullish or bearish trend. Over time, some price trends may become too extended and experience a reversal. Z-scores can be used to measure price deviations from the historical average. While it is difficult to time an exact reversal point, long-term momentum shifts can aid in the gradual rotation away from decaying trends toward emerging trends. We found the MACD/RSI model to produce the best historical results in commodities and equity indices rather than currencies.

Kyaw's ATR/Stochastic model enhances currency trading strategies by combining Average True Range (ATR) and a Stochastic oscillator. ATR measures market volatility, providing insights into the normal price range movements, which helps in setting stop-loss and take-profit levels. The Stochastic oscillator, on the other hand, identifies overbought and oversold conditions, signaling potential reversal points. This combination offers a robust approach to capturing trends and reversals in currency pairs. FX: Recent applications of this model show new long positions in BRL/USD and EUR/GBP, reflecting potential shifts in market dynamics. The BRL/USD pair has demonstrated increasing strength, moving up from a Z-score of -1.04, indicating a potential shift towards a more balanced or bullish sentiment. Similarly, the EUR/GBP pair is near a neutral point with a Z-score of -0.01, suggesting stability and a possible entry point for traders looking for minimal volatility. Both pairs are trading near the bottom of intermediate-term ranges, suggesting that a brief period of mean reversion is possible. Commodities: In the commodities sector, notable changes include Copper Futures, whose Z-score has increased from 1.13 to 1.60, reinforcing the bullish sentiment seen at the end of Q1. This indicates copper prices remain higher than the historical average, driven by expectations of renewed global economic activity. Overall, some commodities are experiencing weaker trends, but we remain on watch for stabilization as bright spots emerge, particularly among active funds that are overweight gold given its long-term breakout. Equities: In global equities, Norway's Oslo Bors (OBX) Index remains above its breakout level achieved in February. The index maintained positive long-term momentum and demonstrated improvement relative to the MSCI Europe Index. The Stoxx Europe 600 Index has shown significant strength, with a Z-score of 2.17, highlighting sustained momentum since the Q4 2023 long entry signaled by the MACD/RSI model. Similarly, the NIKKEI 225 Index has escalated to a Z-score of 2.89, suggesting robust performance relative to historical standards. Conversely, the Hang Seng Index's Z-score improved from -2.34 in Q4 2023 to -1.55 as of the latest data. This improvement might suggest that negative momentum in Chinese and Hong Kong equities is decelerating, potentially nearing a point where a shift from a hold to a buy could be considered. The insights provided by these models and Z-score analyses are instrumental for traders and investors in navigating the complexities of various asset classes, from equities and commodities to currencies. By leveraging such tools, investors can better align their strategies with the prevailing market conditions, optimizing their potential for returns while managing risk. |

Dispersion

Variability of recent price action to its 10-year average, ranked by product.

|

|

|

Portfolio Process

|

Tactical PositioningVictor

|

|

Meet the Team

|

Kyaw Swar

|

Victor

|